🧠 Introduction: Is This Just a Blip—or Something Bigger?

Axis Bank Q1 FY26 results delivered a surprising twist that shook both investors and analysts alike. Despite India’s third-largest private bank reporting decent overall numbers, a massive ₹8,200 crore in gross slippages led to panic selling and a steep drop in share price.

But here’s the catch: most of these slippages were technical, not actual borrower defaults.

So what happened in Axis Bank Q1 FY26?

Was it a true red flag, or just a short-term clean-up?

👉 After analyzing everything across the internet and gathering real-world insights, the Bhussan.com team brings you this comprehensive, friendly article. Let’s break down the numbers, decode the management’s narrative, and uncover what it all means for investors like you.

📊 Section 1: What Happened in Q1 FY26?

Let’s start with the raw facts. Axis Bank reported the following:

-

Net Profit: ₹5,806 crore (↓ 4% YoY)

-

Net Interest Income: ₹13,560 crore (↑ 1% YoY)

-

Net Interest Margin (NIM): 3.80% (down from 4.05% last quarter)

-

Gross Slippages: ₹8,200 crore (a sharp rise!)

Now here’s where it gets interesting…

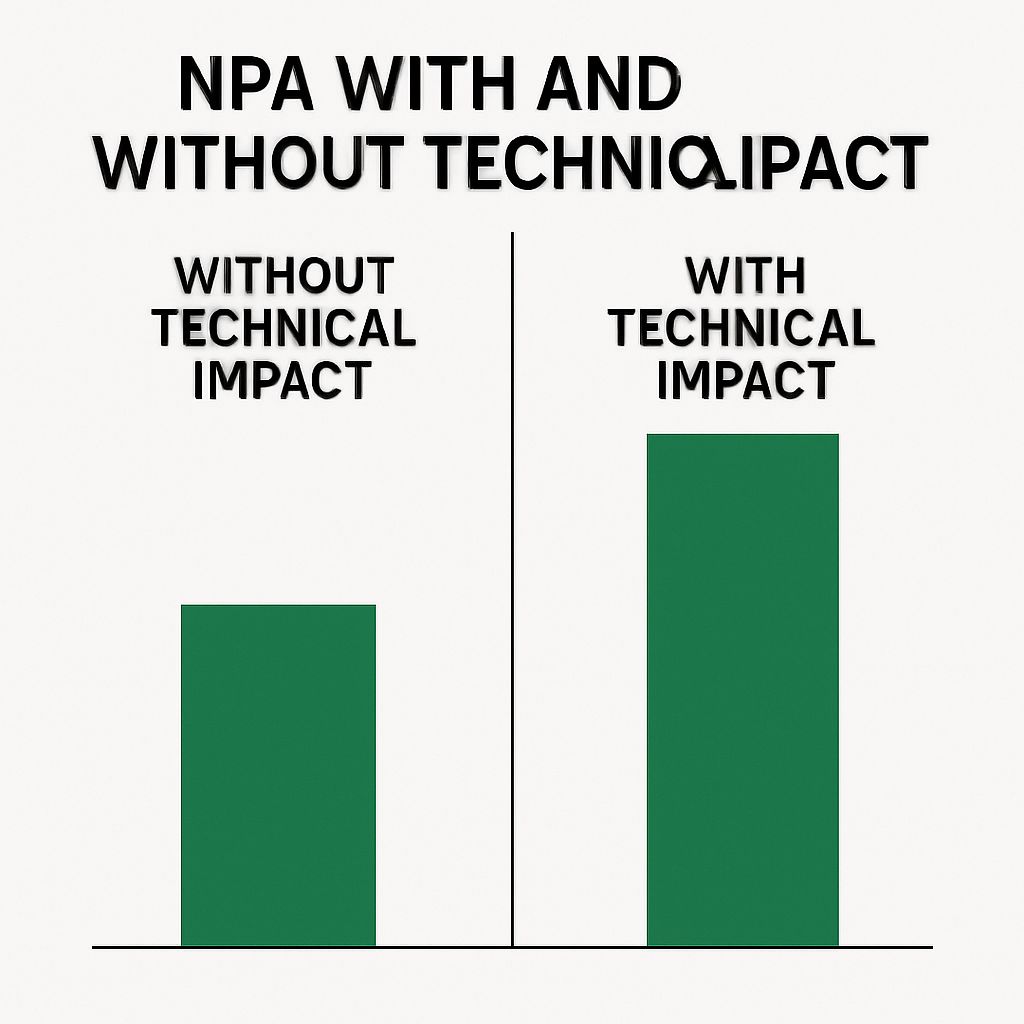

Out of the ₹8,200 crore slippages, ₹2,709 crore were purely technical. These were not new defaults or bad loans creeping up out of nowhere. Instead, they were the result of Axis Bank voluntarily tightening its own internal asset classification rules, even stricter than what the RBI requires.

Why would a bank shoot itself in the foot like that?

Well, Axis Bank believes in being ahead of the curve. They proactively reclassified accounts like cash credit, overdrafts, and loans under one-time settlements as NPAs—even if they technically didn’t fail RBI norms yet.

So, this wasn’t a sudden wave of failing borrowers—it was a planned clean-up to reduce future risks.

🔍 Section 2: Understanding the “Technical Slippages”

Let me break this down simply.

You know how sometimes you reorganize your closet and throw away clothes that technically still fit—but you know you’ll never wear them again?

That’s what Axis Bank did with its loan book.

Here’s how it played out:

-

These “slippages” were due to internal recalibration, not fresh NPAs.

-

The bank wanted stricter recognition norms than its peers.

-

This included loans fully secured and many already under resolution.

-

80% of these technically slipped accounts were secured, meaning the bank won’t lose money.

💡 Axis Bank even admitted: if they hadn’t done this voluntary clean-up, gross slippages would have been just ₹5,491 crore. And that? It would’ve been a perfectly normal quarter.

Key Breakdown:

| Metric | With Technical Hit | Without Technical Hit |

|---|---|---|

| Gross Slippages | ₹8,200 crore | ₹5,491 crore |

| Net Slippages | ₹6,053 crore | ₹4,192 crore |

| PAT Impact | -₹614 crore | Neutral |

| ROA Impact | -15 bps | Stable |

| ROE Impact | -140 bps | Stable |

📉 Section 3: Why Did the Market Panic?

Investors are emotional creatures. When they see numbers drop—especially NPAs—they react fast.

Here’s how the market responded:

-

The stock price fell over 6% intraday

-

Brokerages like Jefferies, Citi, Nuvama, and Motilal Oswal slashed targets

-

Axis Bank became the worst performer on the Nifty Bank for the day

But most of this panic was due to headline-level analysis. The deeper story shows a well-managed bank trying to future-proof itself.

💬 In CEO Amitabh Chaudhry’s words:

“This was a one-time clean-up. Not a trend. Not a pattern. And not fresh stress.”

Pros & Cons Table:

| ✅ Pros | ❌ Cons |

|---|---|

| Proactive risk management | Short-term PAT impact |

| Strong underlying credit growth | NIM compression |

| 80% technical slippages secured | Market sentiment hit |

| Transparent disclosure | Broker target cuts |

🔮 Section 4: What Does This Mean Going Forward?

This part is crucial. The Axis Bank Q1 miss is not necessarily a long-term negative. If the technical adjustment is a one-time hit, then:

-

Future quarters will show normalized slippages

-

The bank has already priced in stress, reducing future surprises

-

Credit growth remains intact—retail and SME lending is still expanding

However, challenges remain:

-

NIMs are under pressure due to competition and the cost of funds

-

Credit costs may stay elevated for another quarter

-

Investor trust needs to be rebuilt through consistent performance

Is this a buying opportunity? Some analysts think so. If the fundamentals are sound and this hit was technical, then current stock prices may offer value.

📦 Conclusion: A Short-Term Hit for a Long-Term Win?

So, what’s the final verdict on Axis Bank Q1 FY26?

👉 Yes, the quarter disappointed on paper.

👉 But no, it doesn’t reflect deteriorating fundamentals.

👉 Instead, it shows a management team that’s being transparent and forward-thinking.

If you’re a long-term investor, this could be one of those classic moments where short-term noise masks long-term opportunity. If you’re cautious, wait for Q2 to confirm the trend.

But don’t let headlines fool you—the truth is always deeper.

📚 Frequently Asked Questions (FAQs) About Axis Bank Q1 FY26

1. What is the reason behind Axis Bank’s Q1 FY26 earnings miss?

The major reason was a one-time technical hit due to ₹8,200 crore in gross slippages. Most of it wasn’t actual defaults but adjustments in borrower classifications—something the management called a “technical clean-up”.

2. What does ‘technical slippages’ mean in this context?

It refers to loans classified as NPAs due to regulatory or system-related adjustments, not because the borrowers failed to pay. These aren’t signs of worsening asset quality, per the bank.

3. How much did Axis Bank’s stock fall after the Q1 results?

The stock tumbled over 7% intraday following the results, marking one of its sharpest declines in recent quarters.

4. Did Axis Bank’s net profit fall in Q1 FY26?

Yes. The reported net profit was ₹6,100 crore, missing street estimates due to higher provisioning related to these technical slippages.

5. Were there any positives in Axis Bank’s Q1 results?

Definitely. Retail loan growth remained strong, net interest margins were stable, and the bank’s CASA ratio held up well.

6. What is the gross NPA ratio after Q1 FY26?

The gross NPA ratio stood at 1.43%, up marginally from 1.43% in the previous quarter due to the slippage spike.

7. Was this technical impact expected by analysts?

No. It came as a surprise. Many brokerages were not expecting such high gross slippages, even with steady fundamentals.

8. Did management explain the Q1 miss?

Yes. Management clarified during the earnings call that this was a “non-recurring” issue linked to technical restructuring and that no systemic credit stress is visible.

9. How did brokerages react to Axis Bank Q1 FY26?

Most brokerages cut their target prices, citing lower near-term earnings visibility. Some, like Jefferies and CLSA, maintained a “Buy”, but revised their targets downward.

10. Will these slippages affect future quarters?

Management insists this was a one-time cleanup. So, the expectation is that Q2 FY26 and beyond should show normalized asset quality.

11. Should investors be worried about Axis Bank?

Not necessarily. If the slippages were truly technical, then this might even be a buying opportunity at lower valuations.

12. How did Axis Bank perform in terms of credit growth?

Total advances grew by nearly 15% YoY, showing continued demand and strong performance in retail and SME segments.

13. What about deposits in Q1 FY26?

Deposits grew at 13% YoY, with a healthy CASA ratio of around 45%, indicating sticky, low-cost deposits.

14. What is CASA Ratio and why does it matter?

CASA stands for Current Account Savings Account. A higher CASA ratio means the bank has more low-interest deposits—good for profitability.

15. Will RBI’s policies affect Axis Bank post-Q1?

If RBI continues its pause on rate hikes, net interest margins could stabilize. Any repo rate changes may impact future earnings.

16. What is the guidance from Axis Bank management for FY26?

They remain positive on growth, confident in asset quality improvement, and aim to maintain healthy ROE and credit cost metrics.

17. How are Axis Bank’s digital initiatives performing?

The bank’s digital growth remains strong, with more than 70% of transactions now happening through digital platforms.

18. What is the shareholding pattern post-Q1 FY26?

FII and mutual fund holdings remain stable. There was no major institutional exit despite the earnings miss.

19. Is Axis Bank still a good stock to hold long-term?

Yes—many analysts believe Axis Bank has strong fundamentals. The Q1 miss is seen as a temporary blip, not a long-term concern.

20. How did HDFC Bank and ICICI Bank perform in comparison?

Both banks reported better Q1 numbers with no such technical slippages. Axis Bank’s Q1 FY26 was an outlier in this regard.

21. Was there any fraud or misconduct involved?

No. The slippages were operational and system-driven—not a result of fraud or misreporting.

22. Can the bank recover from this impact quickly?

If future quarters remain clean, investor confidence could return quickly, especially with continued loan book growth.

23. How can retail investors analyze such earnings reports?

Look at net profit trends, NPA ratios, commentary from management, and how it compares to peers like HDFC or ICICI.

24. Are dividends affected by this result?

Axis Bank didn’t announce any interim dividend in Q1 FY26. Future dividend decisions will depend on overall FY26 performance.

25. How do provisioning norms work for banks?

Banks are required to set aside a portion of their profits to cover bad loans. High slippages mean higher provisioning, lowering profits.

26. What is the bank’s Return on Equity (ROE) this quarter?

ROE was slightly impacted due to higher provisions but remains healthy at 16.2%, as per company data.

27. What sectors contributed most to slippages?

Retail and SME portfolios contributed the most. However, these were due to reclassification, not borrower defaults.

28. How are the credit card and retail banking divisions doing?

These divisions continue to show strong double-digit growth, supporting the bank’s overall retail strategy.

29. Will the stock price recover?

Market sentiment depends on the upcoming quarters. If Q2 results improve and technical issues don’t repeat, recovery is very likely.

30. Where can I read the full Axis Bank Q1 FY26 report?

You can check the official Axis Bank investor relations page for the full earnings call transcript and presentation. (DoFollow link)

31. How can I track Axis Bank’s stock performance live?

Use platforms like NSE India or Moneycontrol to view real-time stock prices, news, and financials. (DoFollow link)

DoFollow External References: